JETRO Invest Japan Report 2025

Chapter2. Trends in Inward FDI to Japan Section5. Cross-Border M&A in Japan

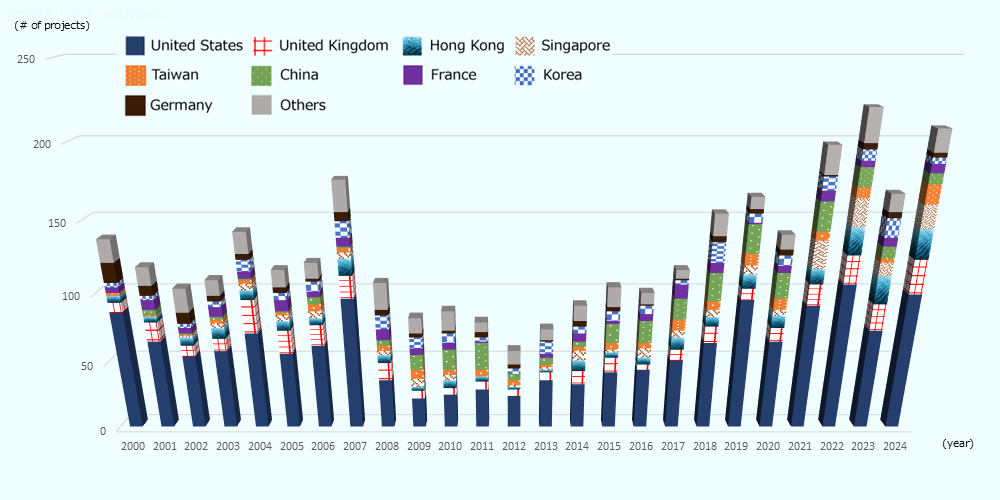

1. Trends in the Number of Deals and Top 5 Countries/ Regions

The number of M&A deals in Japan recovered, with the United States maintaining a dominant lead

In 2024, cross-border M&A transactions targeting Japan in 2024 reached 208 deals, up 24.6% year-on-year, recovering from the decline in 2023 (Chart 2-18). This increase seems to have been driven by factors such as the yen's depreciation making Japanese companies and assets appear undervalued, improvements in the M&A environment through corporate governance reforms, and inflows of capital from overseas private equity funds. By source country/region, the United States ranked first with 99 deals (accounting for 47.6%), followed by the United Kingdom with 24 deals (11.5%) and Hong Kong with 21 deals (10.1%) (Chart 2-19). Singapore rose significantly from 9 to 16 deals, and Taiwan from 3 to 13 deals, while South Korea declined from 13 to 4 deals.

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation. Deals targeting overseas subsidiaries of Japanese companies are excluded.

-

Source:

Based on "MARR Pro" by RECOF DATA Corporation

| Ranking | Co scope="col"untry/Region | 2024 |

2024 Growth rate (YoY) |

2024 Share |

|---|---|---|---|---|

| 1 | United States | 99 | 35.6 | 47.6 |

| 2 | United Kingdom | 24 | 26.3 | 11.5 |

| 3 | Hong Kong | 21 | 5.0 | 10.1 |

| 4 | Singapore | 16 | 77.8 | 7.7 |

| 5 | Taiwan | 13 | 333.3 | 6.3 |

| Total | 208 | 24.6 | 100.0 | |

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation.

Deals targeting overseas subsidiaries of Japanese companies are excluded -

Source:

Based on "MARR Pro" by RECOF DATA Corporation

2. Trends in Deal Value by Investor Country/Region

The U.S. maintains majority share, while the second place and below fluctuate significantly

The total cross-border M&A investment value in Japan over the three-year period from 2022 to 2024 was approximately 7.4 trillion yen, with the top three countries—the United States, Hong Kong, and the United Kingdom—accounting for about 6.1 trillion yen, or 82.6% of the total (Chart 2-20). Looking at trends over consecutive three years on a ten-year interval basis, the total deal value for 2002–2004 stood at approximately 2.2 trillion yen, with the United States alone accounting for 1.8 trillion yen (83.2%) and demonstrating an overwhelming presence. In contrast, the total for 2012–2014 was approximately 1.5 trillion yen, only about 20% of the 2022–2024 figure. This decline reflects the heightened caution toward investments and acquisitions both domestically and internationally, which stems from the global economic slowdown and uncertainty in international financial markets due to European sovereign debt crisis, as well as the disruption of supply chains and deterioration of earnings environment caused by the Great East Japan Earthquake in 2011. Looking at the top countries/regions over this period of over two decades, the United States has consistently maintained its position as the largest investor, but the rankings below have experienced significant fluctuations.

![Three pie charts showing changes in the proportion of cross-border M&A amounts into Japan by country/region across three periods: [2002–2004,] [2012–2014,] and [2022–2024.] * 2002–2004: The US held an overwhelming share at 83.2%. It was followed by Germany (5.6%), the UK (3.4%), Saudi Arabia (2.2%), and France (1.9%), showing a strong tendency towards a unipolar concentration in the US. * 2012–2014: The US continued to be the largest at 64.5%, but its share decreased. It was followed by the UK (11.7%), Thailand (6.7%), Hong Kong (5.9%), and Taiwan (4.7%), showing an increase in the proportion of Asian countries. * 2022–2024: The US stood at 60.0%, with proportions dispersing further. Followed by Hong Kong (11.5%), the UK (11.1%), Saudi Arabia (8.6%), and Sweden (3.1%), indicating a diversification of investment source countries/regions. Overall, it visually shows that while the presence of the US in inward M&A amounts remains significant, the concentration on the US has decreased compared to 20 years ago, with a trend toward a multipolarization of investment entities including Asia, the Middle East, and European countries.](/ext_images/en/invest/img/investment_environment/ijre/report2025/ch2/2-20.png)

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation.

Deals targeting overseas subsidiaries of Japanese companies are excluded. -

Source:

Based on "MARR Pro" by RECOF DATA Corporationme

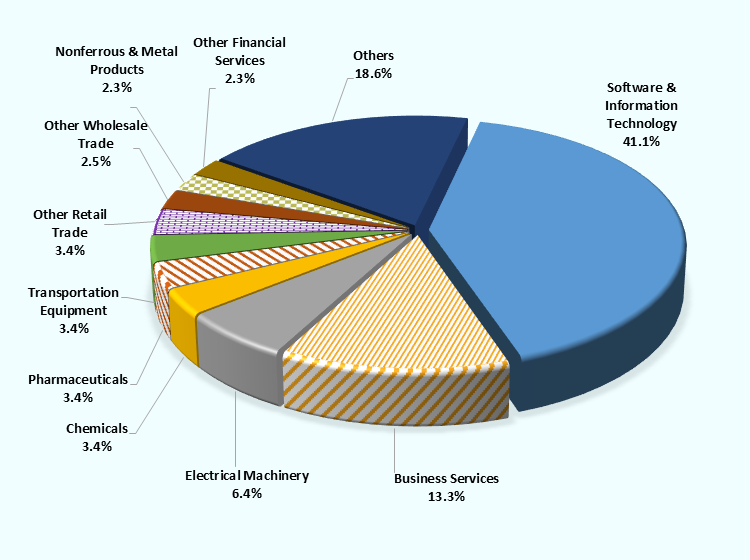

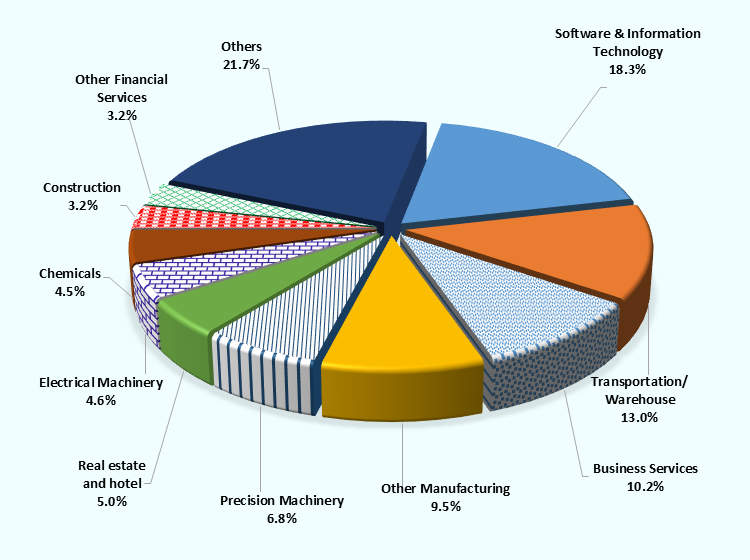

3. Number and Value of Acquired Companies by Industry (Total for 3 Years from 2022 to 2024)

Software and ICT leads in both number and value of deals

Looking at the acquired companies through cross-border M&A in Japan over the three years from 2022 to 2024 by industry, software and ICT led in the number of deals, with 245 (41.1% of the total), followed by services, with 79 (13.3%) and electric machinery, with 38 (6.4%) (Chart 2-21). The top two sectors were both non-manufacturing, which together accounted for over 50% of the total. Software and ICT also led in transaction value, though its share of the total was just under 20%, lower than its share based on the number of deals (Chart 2-22). By contrast, transportation and warehousing, accounted for 13.0% of the total deal value, far exceeding its 1.2% share on a deal-count basis, indicating that the average investment value per transaction in this sector was relatively large.

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation.

Deals targeting overseas subsidiaries of Japanese companies are excluded. -

Source:

Based on "MARR Pro" by RECOF DATA Corporation

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation.

Deals targeting overseas subsidiaries of Japanese companies are excluded. -

Source:

Based on "MARR Pro" by RECOF DATA Corporation

4. Trends in the Value and Number of M&A Deals in Japan

The deal volume is in an established upward trend, while the deal value shows signs of growth again

M&A transactions in Japan are classified into three categories: domestic transactions involving only Japanese parties (IN-IN), inbound transactions where one party is overseas (OUT-IN), and outbound transactions involving Japanese companies acquiring overseas firms (IN-OUT). Based on the three-year moving averages, the analysis on a value basis (left axis) shows that OUT-IN transactions have exhibited a clear upward trend since around 2015, indicating increased activity in large-scale cross-border M&A and private equity investments. IN-IN transactions have also shown an overall increase in value over the same period, gradually expanding their shares.

On a deal-count basis (right axis), the increase in small-scale transactions, such as SME-to-SME M&A via IN-IN deals, is particularly notable, revealing a structure in which small-sized transactions are driving the overall number of deals. As of 2023, IN-IN transactions accounted for approximately 80% of all M&A deals. Meanwhile, IN-OUT and OUT-IN transactions have remained largely flat, with OUT-IN hovering at roughly 50% of IN-OUT.

![A composite graph showing the transition of the amount (in units of 1 billion yen / 10億円) and number of M&A deals involving Japanese companies from 2000 to 2023, broken down by market (IN-IN, IN-OUT, OUT-IN). The bar graph represents the amount (left axis), and the line graph represents the number of deals (right axis), both calculated using a 3-year moving average. * Definition by Market: * IN-IN: M&A between Japanese companies. * IN-OUT: Acquisition of foreign companies by Japanese companies. * OUT-IN: Acquisition of Japanese companies by foreign companies (related to inward FDI). * Transition of Number of Deals (Line Graph): * IN-IN deals: Accounts for the largest proportion, rapidly increasing steadily from a bottom of around 1,000 deals around 2011. Reached a record high level exceeding 3,000 deals in 2023. * IN-OUT and OUT-IN deals: Both hover at levels of 500 deals or fewer, but show a gradual increasing trend over the long term. * Transition of Amount (Bar Graph): * There are major peaks in the mid-2000s and late 2010s. * 2015–2019: A period when amounts swelled significantly. In particular, the amount of [IN-OUT (overseas acquisitions by Japanese companies)] accounted for about half to more than half of the total in many years, with massive acquisitions standing out. * 2020 onwards: Temporarily decreased, but recovered again heading into the most recent year of 2023. In the latest data, [IN-IN] and [IN-OUT] account for the vast majority of the amount, followed by [OUT-IN]. Overall, it visually demonstrates the structure where Japan's M&A market is expanding driven by domestic companies (IN-IN) on a deal-count basis, while on an amount basis, overseas investments by Japanese companies (IN-OUT) significantly influence the market size.](/ext_images/en/invest/img/investment_environment/ijre/report2025/ch2/2-23.png)

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation.

Deals targeting overseas subsidiaries of Japanese companies are excluded. -

Source:

Based on "MARR Pro" by RECOF DATA Corporation

5. Trends in Value and Number of Cross-Border M&A Deals in Japan by Investment Firms

Investment firms' M&A transactions have increased significantly over the past decade

When examining trends in the value and number of cross-border M&A transactions targeting Japan, categorized by investment firms and non-investment operating firms and analyzed using a three-year moving average, it is evident that M&A activity by investment firms has shown a steadily upward trajectory in both deal value and deal count since around 2011 (Chapter 2-24). The transaction value increased approximately elevenfold, from 0.2 trillion yen in 2011 to 2.2 trillion yen in 2023, while the number of transactions rose by about 6.6 times, from 18 deals in 2011 to 118 deals in 2023. Since around 2011, this growth has been driven by an increase in large-scale M&A transactions and private equity investments led primarily by U.S. and European investment firms, alongside increasingly active participation by sovereign wealth funds from regions, such as the Middle East and Singapore.

![A composite graph showing the transition of the amount and number of inbound M&As (OUT-IN) by overseas [Investment Companies] and [Non-Investment Companies] from 2000 to 2023. The bar graph represents the amount (left axis: in units of 1 billion yen), and the line graph represents the number of deals (right axis: in deals), both calculated using a 3-year moving average. * Transition of Number of Deals (Line Graph): * Investment Companies: Surged from less than 10 deals in the early 2000s towards the mid-2010s. Reached approximately 120 deals in the most recent year of 2023, continuing to break record highs. * Non-Investment Companies: Decreased once from about 110 deals in the early 2000s, but started increasing again around 2013. Recovered to about 80 deals in 2023. Since 2018, the number of deals by investment companies has continuously exceeded those by non-investment companies. * Transition of Amount (Bar Graph): * Investment Companies: The amount scale expanded rapidly from the late 2010s. It is particularly noticeable from 2020 onwards, with acquisition amounts by investment companies reaching a scale of approximately 2.2 trillion yen (2,200 billion yen) in 2023, accounting for the vast majority of the entire market. * Non-Investment Companies: Maintained a certain presence in the 2000s and early 2010s, but their relative contribution on an amount basis has become smaller in recent years. Overall, it visually demonstrates that in the recent inward M&A market, investments by overseas investment companies (such as private equity funds) have rapidly increased their presence in both the number of deals and amounts, becoming the main driver of current inward FDI (M&A type).](/ext_images/en/invest/img/investment_environment/ijre/report2025/ch2/2-24.png)

-

Note:

Transaction forms include mergers, acquisitions, business transfers (including operational transfers), and capital participation.

Deals targeting overseas subsidiaries of Japanese companies are excluded. -

Source:

Based on "MARR Pro" by RECOF DATA Corporation

6. Major Cross-Border M&A Deals in Japan (January 2024 to September 2025, based on announcement date)

M&A led by investment firms accounts for the majority of transactions

As in 2023, management buyout (MBO) deals led by investment firms stood out as a prominent form of M&A transactions (Chart 2-25). The motives, purposes, and methods of transactions have become increasingly diverse, including the business transfers of York Holdings and Mitsubishi Tanabe Pharma, the prolonged stakeholder alignment required for Fuji Soft's successful TOB, compliance with national security reviews under the Foreign Exchange and Foreign Trade Act for Shibaura Electronics, and capital participation in companies such as Kao, Sanwa Holdings, Tokyo Gas, NEC Networks & System Integration, and Shiseido.

|

Target company (Transferring entity) |

Target company: Sector |

Acquiring company (Substantial acquiring entity *Note 1) |

Acquiring company: Country/region of the acquiring company's ultimate parent company | Acquiring company: Sector | Form | Outline |

Publication date (Effective date) *Note 2 |

Values (100 million JPY) *Note 3 |

|---|---|---|---|---|---|---|---|---|

| York Holdings Co., Ltd. | Retail trade |

BCJ-96 (Receiving company) (Bain Capital) |

U.S. |

Other finance (Investment fund) |

Transfer of business | Bain Capital, through its acquisition vehicle BCJ-96, acquired by way of a company split all rights and obligations related to the SST (superstore) business from York Holdings, a wholly-owned subsidiary of Seven & i Holdings Co., Ltd., which holds Ito-Yokado, York Benimaru (Koriyama, Fukushima), and other SST operations. Bain Capital aims to achieve an IPO by maximizing the potential value of the SST business group. The Seven & i Holdings will advance its growth strategy centered on the convenience store business. |

2025/3/7 (2025/9/1) |

8,147 |

| FUJI SOFT INCORPORATED | Information and communications |

FK (Acquisition company) (Fund managed by Kohlberg Kravis Roberts & Co. [hereafter, KKR]) |

U.S. |

Other finance (Investment fund) |

Acquisition | U.S. investment fund KKR took FUJI SOFT private through a two-step tender offer bid (TOB) conducted by FK established by FK Holdings, a corporation wholly owned by a fund managed by KKR. FUJI SOFT determined that partnering with KKR, which has human and capital resources, proven track records in both the IT and real estate fields, and a global network, would enable the company to achieve dramatic growth. |

2024/8/9 (2025/5/20) |

6,060 |

|

Mitsubishi Chemical Group Corporation (Parent company of Mitsubishi Tanabe Pharma Corporation, the target of transfer) |

Chemicals (Pharmaceuticals) |

BCJ-94 (Receiving company) (Fund advised in investment by Bain Capital) |

U.S. |

Other finance (Investment fund) |

Transfer of business | BCJ-94, a corporation funded by a fund that is advised in investment by U.S. investment fund Bain Capital, took over all the shares and related assets of Mitsubishi Tanabe Pharma from Mitsubishi Chemical Group through a corporate split. The purpose of this M&A is to establish a system that enables Mitsubishi Tanabe Pharma to develop its business more flexibly and swiftly, aiming to enhance its pharmaceutical expertise and strengthen its competitiveness in the global market. Bain Capital emphasizes growth potential in the pharmaceutical sector and aims to optimize management resources and increase business value while ensuring Mitsubishi Tanabe Pharma's independence. | 2025/2/8 | 5,100 |

| TOPCON CORPORATION | Precision equipment |

TK (Acquisition company) (Funded by the following: a fund managed by KKR, TOPCON's management, and a fund managed by JIC Capital, a subsidiary of Japan Investment Corporation) |

U.S. |

Other finance (Investment fund) |

Acquisition (MBO) | The president of TOPCON, in collaboration with U.S. investment fund KKR, acquired TOPCON itself through a management buyout (MBO), and the company became a wholly owned subsidiary through a TOB conducted via TK, which is an acquisition company established by TK Holdings (TKHD) fully owned by a fund managed by KKR. Following the completion of the TOB, JIC Capital, a wholly-owned subsidiary of the Japan Investment Corporation, will invest a total of 95 billion yen through a fund it manages by underwriting preferred shares of TKHD. TOPCON designs, manufactures, and sells optical and device products for the space and defense industries. Leveraging KKR's global human and capital resources, TOPCON will not only enhance its own capabilities, but also implement measures to grow sales and improve profitability by supporting diversified growth strategies, including collaboration with outside parties and acquisitions. | 2025/3/29 | 3,482 |

| INFOCOM CORPORATION | Information and communications |

PXJC2 Holding (Acquisition company) (Fund managed by the Blackstone Group) |

U.S. |

Other finance (Investment fund) |

Acquisition | The Blackstone Group, a U.S. investment fund, acquired INFOCOM, a subsidiary of TEIJIN, that operates the smartphone-based digital comic distribution service Mecha Comic, through a TOB conducted by PXJC2 Holding, which was established with full funding from a fund managed by Blackstone. Blackstone plans to leverage the expertise and network of its portfolio company, U.S.-based Candle Media, to provide support to accelerate INFOCOM's overseas expansion and monetization through the utilization of its intellectual property. TEIJIN is seeking to reform its business portfolio. |

2024/6/19 (2024/10/18) |

2,760 |

| ALPS LOGISTICS CO., LTD. | Transportation and warehousing |

LDEC (Acquisition company) (LOGISTEED: 90% owned by KKR) |

U.S. | Transportation and warehousing | Acquisition | LOGISTEED (formerly Hitachi Transport System), a logistics company backed by U.S. investment fund KKR, acquired ALPS LOGISTICS through a TOB conducted via its wholly owned subsidiary LDEC. This acquisition enables them to provide high value-added and efficient logistics services consistent from procurement logistics to finished goods logistics, expand the customer base, realize economies of scale through increased logistics volume, and advance system development to a higher level. |

2024/5/9 (2024/12/19) |

1,761 |

| Kao Corporation | Chemicals (Cosmetics) | Oasis Management Company | British Cayman Islands |

Other finance (Investment fund) |

Capital participation | Oasis Management Company, an investment fund registered in the British Cayman Islands, with an operational base in Hong Kong, has acquired a stake in Kao (purchasing 5.23% of its outstanding shares). The purpose of the holding stake is stated as portfolio investment and making significant proposals. On April 1, 2025, Oasis issued a statement titled a better Kao, calling for a greater focus on global expansion and a review of its brand portfolio. | 2024/12/11 | 1,489 |

| T-Gaia Corporation | Other sales and wholesale |

BCJ-82-1 (Acquisition company) (Fund managed by Bain Capital) |

U.S. |

Other finance (Investment fund) |

Acquisition | A fund managed by U.S. investment fund Bain Capital acquired T-Gaia, a major mobile phone sales agency, by conducting a TOB via BCJ-82-1, a wholly owned subsidiary of the fund. T-Gaia had been operating retail stores nationwide for carriers such as NTT DOCOMO and KDDI, but the business environment became increasingly challenging due to factors including the lengthening mobile phone replacement cycle. Bain Capital, leveraging its investment expertise in the retail and consumer industries, will support T-Gaia in enhancing the profitability of its mobile business, strengthening its corporate sales operations, accelerating growth through additional M&A, and bolstering its execution capabilities to achieve growth. |

2024/10/1 (2025/03/05) |

1,426 |

| Japan KFC Holdings | Retail trade (Food and beverage) |

Krispy (Acquisition company) (Fund managed by Carlyle Group) |

U.S. |

Other finance (Investment fund) |

Acquisition | Carlyle Group, a U.S. investment fund, has acquired KFC Holdings Japan through a TOB conducted via Krispy, a wholly owned subsidiary of the Carlyle Group. KFC Holdings Japan became a subsidiary of Mitsubishi Corporation through a TOB in 2007 and subsequently sold a portion of its shares in 2015. Carlyle will accelerate new store openings and increase earnings at each store. |

2024/5/21 (2024/09/20) |

1,350 |

| NISSIN CORPORATION | Transportation and warehousing |

BCJ-98 (Acquisition company) (Fund managed by Bain Capital, NISSIN's current management team) |

U.S. |

Other finance (Investment fund) |

Acquisition (MBO) | The U.S. investment fund Bain Capital acquired NISSIN, a comprehensive logistics company with NISSIN's side through a management buyout (MBO) via a TOB executing by BCJ-98, a company established and fully owned by a fund that is advised in investment by Bain Capital. NISSIN provides international multimodal transportation services that optimally combine all modes of transportation: land, sea, and air. By leveraging Bain Capital's global network, human resources network, and management expertise, the company aims to promote management reforms in a flexible and agile manner. |

2025/5/13 (2025/07/15) |

1,183 |

| SHIBAURA ELECTRONICS | Electric machinery |

YAGEO Electronics Japan LLC (Acquisition company) (Yageo Corporation) |

Taiwan | Electric machinery | Acquisition (TOB) | YAGEO, a major Taiwanese electronic component manufacturer, conducted a tender offer bid (TOB) for shares of SHIBAURA ELECTRONICS through its acquisition company YAGEO Electronics Japan LLC. SHIBAURA ELECTRONICS specializes in the development, manufacturing, and sales of thermistor elements and temperature sensors, and has a strong foundation of trust and a customer network within Japan. YAGEO stated that the purpose of the acquisition is to maintain SHIBAURA ELECTRONICS's domestic foundation and support its business expansion leveraging YAGEO's international channels. Although YAGEO extended the TOB period multiple times due to national security reviews under Japan's Foreign Exchange and Foreign Trade Act, the TOB was ultimately completed after satisfying all legal requirements. |

2025/2/6 (2025/7/8) |

1,089 |

| Samty Holdings Co., Ltd | Real estate and hotels |

Song Bidco G.K. (Acquisition company) (Fund managed by Hillhouse Investment Management) |

Hong Kong |

Other finance (Investment fund) |

Acquisition | Hillhouse Investment Management, an alternative investment management firm based in Singapore and China, acquired Samty Holdings through a TOB conducted via Song Bidco G.K., which is wholly owned by a fund managed, advised and operated by Hillhouse. Hillhouse has an investment strategy centered on real estate, and will expand its real estate business in Japan, while Samty Holdings aims to shift its revenue structure from one focused on capital gains to one that expands income gains through rental income generated from its planned and developed income-producing properties. Additionally, the company will utilize third-party capital to form real estate development funds and core funds, and strengthen its asset management business. |

2024/10/12 (2025/02/03) |

1,068 |

| NIHON HOUSING CO., LTD. | Real estate and hotels |

Marcian HOLDINGS LLC (Acquisition company) (Goldman Sachs, NIHON HOUSING's current management team) |

U.S. | Securities | Acquisition (MBO) | NIHON HOUSING, in collaboration with Goldman Sachs of the U.S., conducted a TOB via Marcian HOLDINGS LLC to delist the company through an MBO. NIHON HOUSING operates condominium business, building management business, and real estate management business. The company aims to rebuild its business foundation by leveraging Goldman Sachs' accumulated expertise and insights in the real estate development and facility management businesses, global and diverse real estate portfolio and network, as well as capabilities in providing strategic support and proposals related to M&A and business strategy. |

2024/5/9 (2024/09/04) |

944 |

| TRANCOM CO., LTD. | Transportation and warehousing |

BCJ-86 (Acquisition company) (Fund managed by Bain Capital, TRANCOM's current management team) |

U.S. |

Other finance (Investment fund) |

Acquisition (MBO) | TRANCOM, a major logistics company, jointly conducted a TOB via BCJ-86, wholly owned by a fund that is advised in investment by U.S. investment fund Bain Capital, and it was taken private through a management buyout (MBO). TRANCOM is working to fundamentally improve logistics efficiency in response to changes in the business environment, including the so-called 2024 problem, where restrictions on drivers' overtime hours are expected to lead to a shortage in transportation capacity. By leveraging Bain Capital's global network, experience in driving growth through M&A, human resources network, and management expertise, the company aims to promote management reforms in a flexible and agile manner. |

2024/9/18 (2025/01/17) |

911 |

| JTOWER Inc. | Information and communication |

DB Pyramid Holdings LLC (Acquisition company) (Fund managed by Digital Bridge Group) |

U.S. |

Other finance (Investment fund) |

Acquisition | Digital Bridge Group, a U.S. digital infrastructure investor, acquired JTOWER, a telecommunications infrastructure sharing business, through a TOB conducted via DB Pyramid Holdings LLC, a wholly owned U.S. subsidiary of Digital Bridge Group. The company has a proven track record of supporting global telecommunications networks. JTOWER seeks to strengthen its management foundation by adding Digital Bridge as a new partner. Following the TOB, the company aims to improve its competitive advantage by enabling swift decision-making and more flexible investment strategies through delisting, while accelerating the development of the infrastructure sharing business and strengthening cooperation with domestic telecom carriers and partner companies. |

2024/8/15 (2025/01/09) |

760 |

| Sanwa Holdings Corporation | Nonferrous and metal products | Value Act Capital Management, L.P. | U.S. |

Other finance (Investment fund) |

Capital participation | Value Act Capital Management, L.P., an activist hedge fund based in San Francisco, acquired a 5.94% stake in Sanwa Holdings, a leading building materials company engaged in mainly producing shutters, doors for buildings and condominiums, and aluminum storefront system. The stated purpose of the holding stake is to give advice on investment and management, and make important proposals according to circumstances. Going forward, the company will propose management strengthening measures to accelerate growth, such as improving management efficiency, optimizing capital policies, developing new markets, and reviewing the business portfolio. Sanwa Holdings is expected to strengthen its competitiveness by utilizing the overseas investor network and management expertise. | 2024/9/26 | 667 |

| Roland DG Corporation | Electric machinery |

XYZ (Acquisition company) (Fund managed by Taiyo Pacific Partners, Roland DG's current management team) |

U.S. |

Other finance (Investment fund) |

Acquisition (MBO) | Jointly with U.S. investment firm Taiyo Pacific Partners, Roland DG, a commercial printer manufacturer, conducted a TOB via XYZ, a company established by a fund managed and operated by Taiyo Pacific Partners, and subsequently took Roland private via a management buyout (MBO). The company is shifting away from a business structure that relies on low-solvent printers for the signage market, which accounts for about 40% of its sales, and is accelerating growth by promoting corporate reforms that utilize external management resources. |

2024/2/9 (2024/09/05) |

664 |

| TOKYO GAS CO., LTD | Electricity and gas | Elliott Investment Management L.P. | U.S. |

Other finance (Investment fund) |

Capital participation | U.S. activist fund Elliott Investment Management L.P. acquired approximately 5% of Tokyo Gas shares and is urging the company to improve management efficiency and strengthen its capital policy. Tokyo Gas is taking measures focused on improving capital efficiency and enhancing corporate value, and announced plans to repurchase up to 40 billion yen worth of its own shares and to consider selling non-core assets, such as real estate. The company has clearly stated its intention to allocate the proceeds to growth investments and shareholder returns. Top management emphasizes its commitment to optimizing the business portfolio and enhancing competitiveness through constructive dialogue with external shareholders. | 2024/11/20 | 650 |

| NEC Networks & System Integration Corporation | Information and communications | Oasis Management Company | Hong Kong |

Other finance (Investment fund) |

Capital participation | Oasis Management Company, an investment fund registered in the British Cayman Islands, with an operational base in Hong Kong, has acquired a stake in NEC Networks & System Integration (purchasing 6.01% of its outstanding shares). The purpose of the holding stake is stated as portfolio investment and making significant proposals. Subsequently, Oasis increased its shareholding through on-market transactions, raising its stake to 10.42% and then to 13.12%. At the time NEC announced the completion of its TOB, Oasis had further increased its stake to 15.22%. | 2024/11/7 | 595 |

| Shiseido Company | Chemicals (Cosmetics) | Independent Franchise Partners, LLP | U.K. |

Other finance (Investment fund) |

Capital participation | Independent Franchise Partners, an investment management firm based in London, U.K., has acquired 5.2% of Shiseido's common stocks. In response, Shiseido is promoting structural reforms to improve profitability by undertaking initiatives to identify areas for improvement in earnings and capital efficiency by business unit, while visualizing their respective contributions to overall corporate value. Going forward, the company plans to expand these reforms globally and establish a sustainable profit structure. Management is actively communicating its results and plans, and appealing to shareholders and the market about its ability to execute and its commitment to increasing corporate value. | 2025/2/20 | 581 |

-

Note1:

If the tender offeror is an SPC (special purpose company), etc., the substantive acquiring entity is also listed.

-

Note2:

The "announcement date" refers to the date on which the transaction was disclosed to the public through news releases, newspaper articles, or similar sources, and the "effective date" refers to the date on which the deal was completed (including scheduled completion dates).

For transactions categorized as "capital participation," these transactions had already been completed as of the announcement date. -

Note3:

In order of investment amount based on company announcements or media reports.

-

Source:

Based on "MARR Pro" by RECOF DATA Corporation

JETRO Invest Japan Report 2025

-

Section1

-

Section2

-

Section3

-

Section4

-

Section1

-

Section2

-

Section3

-

Section4

-

Section5

-

Section1

-

Section2

-

Section3

Laws and Regulations on Setting Up Business in Japan Pamphlet

The pamphlet "Laws & Regulations" is available in PDF, and outlines basic information about laws, regulations and procedures related to setting up a business in Japan. It is available in English and Japanese. You can download via the "Request Form" button below.

Contact Us

Investing in and collaborating with Japan

We will do our very best to support your business expansion into and within Japan as well as business collaboration with Japanese companies. Please feel free to contact us via the form below for any inquiries.

Inquiry FormJETRO Worldwide

Our network covers over 50 countries worldwide. You can contact us at one of our local offices near you for consultation.

Worldwide Offices