JETRO Invest Japan Report 2025

Chapter2. Trends in Inward FDI to Japan Section4. Greenfield Investment in Japan

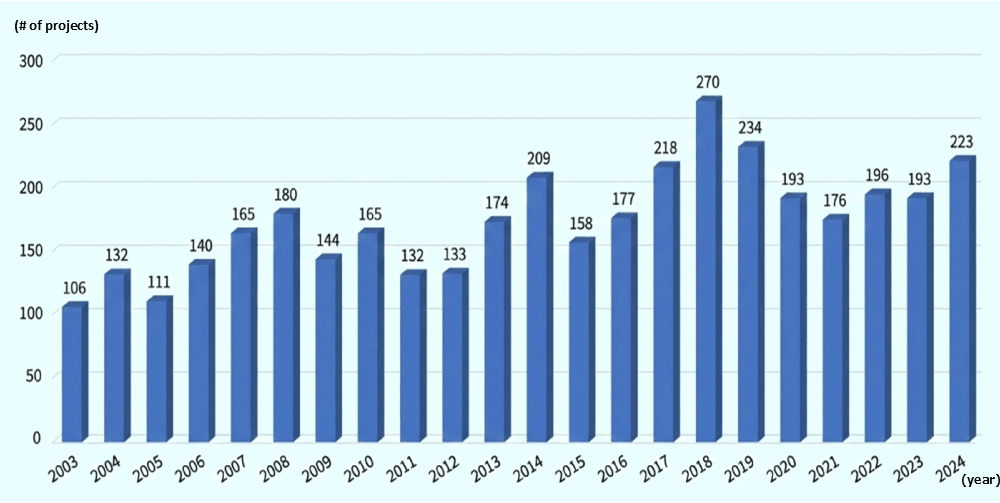

1. Trends in the Number of Investments

Notable increases observed in sectors of communications, semiconductor chips, and electronic components

In 2024, the number of greenfield investments in Japan (based on announcement date) was 223, up 15.5% from the previous year (Chart 2-11). While the global total of greenfield investments (19,356) increased only 2.9% from the previous year, Japan saw solid performance in sectors of communications, semiconductor chips, and manufacturing of electronic components, devices, and electronic circuits, and these three sectors combined accounted for 50 cases, up 18 from the previous year, representing a 22.4% share.

-

Note:

The number of investments is collected continuously based on company announcements and updated at the end of each month. Figures include cases where the investment destination region or prefecture is unknown.

-

Source:

Based on "fDi Markets" by the Financial Times

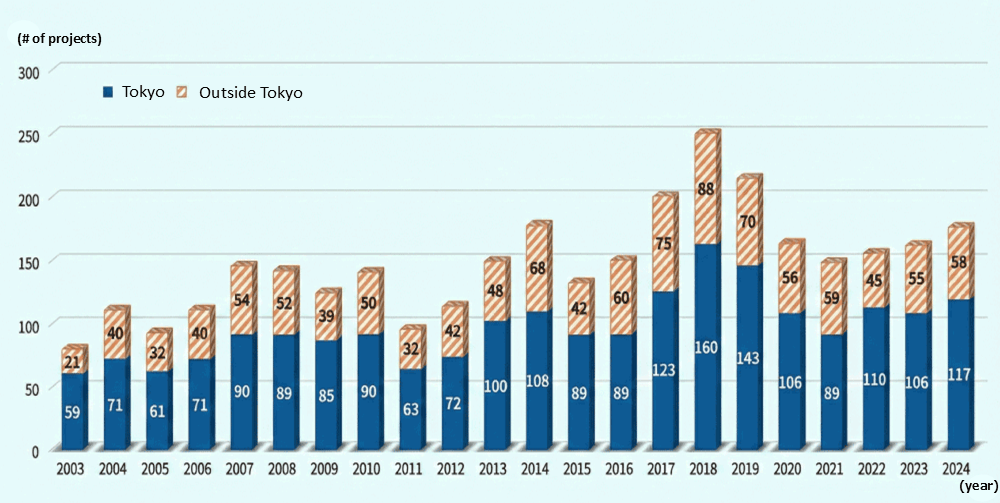

2. Number of Investments by Destination Region (Tokyo and Other Regions)

Investment projects in Tokyo accounted for about 70%

Dividing greenfield investment projects in Japan (based on announcement dates) where the destination region (prefecture) is known, into Tokyo and other regions, there were 117 cases in Tokyo and 58 cases in other regions in 2024 (Chart 2-12). The share of Tokyo has generally remained at around 60–70% over the past two decades.

-

Note:

Figures exclude cases where the investment destination region or prefecture is unknown.

-

Source:

Based on "fDi Markets" by the Financial Times

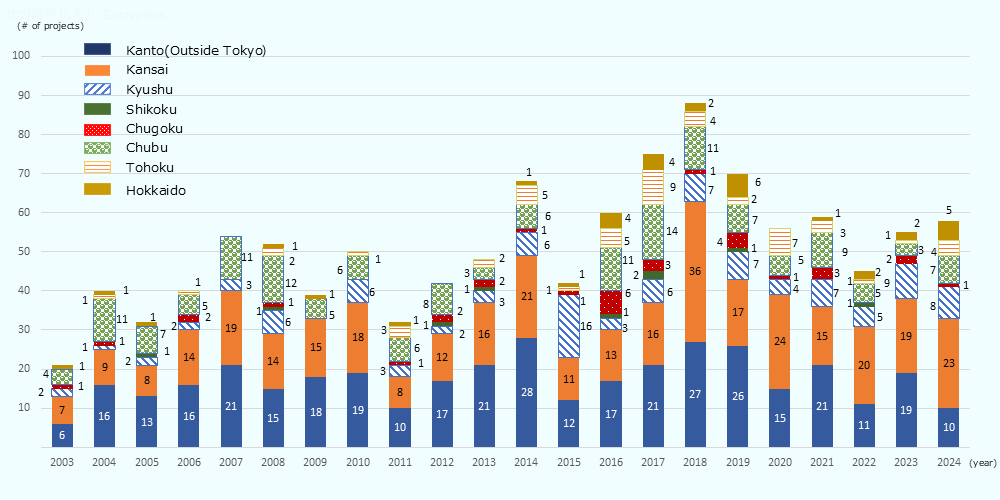

3. Trends in the Number of Investments by Destination Region (Breakdown of Regions Other Than Tokyo)

Outside the Kanto region, each region in Kansai and further east exceeded their 2023 level

Looking at greenfield investment projects in Japan (based on announcement date) where the destination region (prefecture) is known—excluding Tokyo, in 2024, the Kansai region recorded 23 cases, up 4 from the previous year, Chubu had 7 cases, up 4, Hokkaido had 5 cases, up 3, and Tohoku had 4 cases, up 3, all showing year-on-year increases (Chart 2-13). On the other hand, the Kanto region excluding Tokyo saw a decrease of 9 cases to 10, Kyushu fell by 1 to 8, and Chugoku declined by 1 to 1, compared to 2023, indicating regional differences.

-

Note:

: Figures exclude cases where the investment destination region or prefecture is unknown. The Kanto region (other than Tokyo) includes six prefectures; Ibaraki, Kanagawa, Gunma, Saitama, Chiba, and Tochigi.

-

Source:

Based on "fDi Markets" by the Financial Times

4. [Reference] Analysis of Spillover Effects of Greenfield Investment in Japan

A 2 trillion yen investment in Tokyo generates 600 billion yen spillover investment in other regions

Of the 223 greenfield investment projects in Japan in 2024 (based on announcement date), 166 projects for which the destination region (prefecture) is known[*note]—with a total value of 21.1 billion US dollars (approximately 3.2 trillion yen)—were analyzed to estimate spillover investment amounts to other regions for direct investment in each prefecture. The results showed that investments of 19.8 billion US dollars (approximately 3.0 trillion yen) had been induced in regions other than the primary destination. Investment destinations were concentrated in the Kanto region, with Tokyo accounting for 74.7% of the total at 14.8 billion US dollars (approximately 2.2 trillion yen). Calculating the spillover effects of the investment in Tokyo, it induced 10 billion US dollars (approximately 1.5 trillion yen) within Tokyo and 4 billion US dollars (approximately 0.6 trillion yen) in other regions (Chart 2-14). Regions highly responsive to Tokyo-origin investments could expect additional spillover amounts by improving conditions for receiving such investments (e.g., industrial structure and incentives).

-

[*note]

Nine projects with inconsistencies in the spillover effect calculations were excluded from the analysis, leaving 166 projects for the trial estimate.

![A bubble chart showing the relationship between the spillover investment amount and the Tokyo Spillover Index (TSI) in each prefecture. The horizontal axis is the spillover amount (unit: 100 millions of yen) ranging from 0 to 3,500 (100 millions of yen), and the vertical axis indicates the spillover intensity of investments originating from Tokyo, with a scale from −1.0 to 5.0. The size of the bubbles indicates the investment scale of each region. * Definition of Tokyo Spillover Index (TSI): A ratio that relatively expresses the strength of linkage with Tokyo, defined by the formula [Spillover amount originating from Tokyo ÷ Spillover amount originating from outside Tokyo.] A value greater than 1 means a high degree of spillover/linkage from Tokyo, while less than 1 means spillovers from outside Tokyo are larger. * Distribution Status: * Regions with large spillover amounts and low TSI: Osaka stands out with a large spillover amount of approximately 2,700 (100 millions of yen), but its TSI is low at under 0.5, indicating that spillovers from outside Tokyo are dominant. Regions like Kanagawa, Aichi, Saitama, Ibaraki, and Hokkaido also exceed 1,000 in spillover amounts, while their TSI remains at 1.5 or below. * Regions with small spillover amounts but high TSI: Regions such as Oita, Nagano, Fukushima, Miyagi, Ehime, and Yamagata have small spillover amounts themselves (under 500), but their TSI is very high ranging from 2.5 to 4.0, showing a strong tendency for investments to be linked to Tokyo's movements. * Intermediate regions: Chiba has a spillover amount of about 700 and a TSI of about 2.0, possessing both a substantial spillover amount and linkage with Tokyo. Overall, it visually demonstrates a correlation where regions with larger spillover investment amounts tend to have their own unique spillover pathways outside of Tokyo, while conversely, regions with relatively small-scale spillover amounts strongly rely on investment spillovers from Tokyo.](/ext_images/en/invest/img/investment_environment/ijre/report2025/ch2/2-14.png)

-

Explanation of Chart:

1. Nationwide Secondary Core Type (Osaka)

Representative: Osaka

Criteria: Osaka only (Spillover Amount: 264.7 billion yen)

Osaka is Japan's second-largest core city after Tokyo. It has overwhelming scale and an independent acceptance structure, occupying the position of a secondary core.2. Nationwide Cluster Type (Hubs)

Representative: Aichi, Kanagawa

Criteria: TSI ≥ 1.0 and Spillover Investment Amount > 105 billion yen

A cluster that receives spillovers on a nationwide scale. Backed by industrial cluster and major urban functions, it plays a role in inducing investment across the country.3-1. Regional Core Type (Independent)

Representative: Hokkaido, Ibaraki, Shizuoka, Fukuoka, Okayama

Criteria: Independent type (TSI < 1) and medium-scale spillover amount (30.0–105.0 billion yen)

Serves as the center of a regional block without relying on linkage with Tokyo.3-2. Regional Core Type (Linked)

Representative: Saitama, Chiba, Hyogo

Criteria: Linked type (TSI ≥ 1.0) and medium-scale spillover amount (30.0–105.0 billion yen)

Supports the regional economy while remaining linked to spillovers originating from Tokyo.4. Others (small-scale, highly linked regions) Representative: Nagano, Oita, Fukushima, Miyagi, Yamagata, Ehime, etc.

Criteria: Generally, TSI ≥ 2.0 and spillover investment amount of 30.0 billion yen or less

These regions exhibit relatively high linkage to spillovers originating from Tokyo. Because they are small-scale prefectures, the effect of direct investment from Tokyo is observed to be relatively large. -

Note:

Exchange rate: ¥151.48/USD (2024 fiscal year conversion rate based on the Bank of Japan website, Tokyo interbank market, USD/JPY spot rate, monthly average of central rates). The bubble size corresponds to the X-axis and visualizes the spillover amount.

-

Source:

Based on "Inter-Prefectural Input-Output Table (26 sectors)" by the Ministry of Economy, Trade and Industry

5. Top 10 Countries/Regions and Top 10 Industries

By country, the United States accounts for just over 30%, far surpassing all others

Looking at the number of greenfield investments in Japan in 2024 (based on announcement date) by source country/region, the United States had the most with 71 cases, up 10.9% from the previous year (Chart 2-15). Singapore, which ranked second in 2023, fell from 21 to 16 cases and dropped to third place. The United Kingdom, previously third, edged down slightly 18 to 17 cases, but moved up to second place. As in 2023, China ranked fourth and Hong Kong ranked fifth. Broken down by industry, software & IT services remained the leading sector, as in 2023, with a 2.7% year-on-year increase (Chart 2-16). Sectors with the largest growth rates included communications (+84.6%), renewable energy (+83.3%), and electrical components (+66.7%). Those with the largest declines were financial services (-23.1%) and industrial equipment (-37.5%).

| Ranking | Country/Region | 2024 |

2024 Growth rate (YoY) |

2024 Share |

|---|---|---|---|---|

| 1 | United States | 71 | 10.9 | 31.8 |

| 2 | United Kingdom | 17 | 0.0 | 7.6 |

| 3 | Singapore | 16 | -23.8 | 7.2 |

| 4 | China | 14 | 27.3 | 6.3 |

| 5 | Hong Kong | 12 | 100.0 | 5.4 |

| 6 | Germany | 8 | 60.0 | 3.6 |

| 7 | Canada | 6 | 50.0 | 2.7 |

| 7 | France | 6 | 50.0 | 2.7 |

| 9 | South Korea | 3 | -25.0 | 1.3 |

| 9 | Switzerland | 3 | -40.0 | 1.3 |

| Total | 223 | 15.5 | 100.0 | |

-

Source:

Based on "fDi Markets" by the Financial Times

| Ranking | Sector | 2024 |

2024 Growth rate (YoY) |

2024 Share |

|---|---|---|---|---|

| 1 | Software & IT services | 38 | 2.7 | 17.0 |

| 2 | Business services | 34 | 6.3 | 15.2 |

| 3 | Communications | 24 | 84.6 | 10.8 |

| 4 | Financial services | 20 | -23.1 | 9.0 |

| 5 | Real estate | 18 | 12.5 | 8.1 |

| 6 | Electronic components | 15 | 66.7 | 6.7 |

| 7 | Transportation & Warehousing | 11 | 10.0 | 4.9 |

| 7 | Renewable energy | 11 | 83.3 | 4.9 |

| 9 | Industrial equipment | 10 | -37.5 | 4.5 |

| 9 | Semiconductors | 10 | 0.0 | 4.5 |

| Total | 223 | 15.5 | 100.0 | |

-

Source:

Based on "fDi Markets" by the Financial Times

6. Major Greenfield Investment Projects in Japan (January 2024 to September 2025, based on announcement date)

Large-scale projects for data centers and logistics facilities stand out

Looking at greenfield investment projects in Japan from January 2024 to the end of Q3 2025, while large-scale projects such as the construction of production plants by major semiconductor manufacturers were notable in 2023, this period has seen a series of announcements for data center and logistics facility construction projects, with a significant increase in the number of cases (Chart 2-17).

| Company name | Country/Region | Sector | Investment destination (prefecture) | Outline | Date (Based on announcement / media reports) | Value(Million US$) |

|---|---|---|---|---|---|---|

| Ada Infrastructure | Singapore | Communications | Tokyo and Kansai regions | Ada Infrastructure is a global data center (DC) business brand launched in September 2023 by Singapore-based logistics facility developer GLP. The company announced the projects of two DCs in the Tama area of Tokyo, two DCs in Chiba, a DC in Kansai region. Overall, it plans to build DCs with a total IT power of 600MW (a supply capacity of 900 MW). The one in the Tama area has already launched and the others will be in operation around 2027-2028. | May 2024 | 11,760 |

| Patience Capital Group | Singapore | Leisure and Entertainment | Niigata | In November 2023, Singapore-based Patience Capital Group acquired Myoko Suginohara Ski Resort in Niigata Prefecture and entrusted its operation to Seibu Holdings. The company has announced plans to invest a total of 200 billion yen to redevelop Myoko Kogen as a year-round resort. | March 2025 | 1,343 |

| ESR | Hong Kong | Real Estate | Hyogo | ESR, a leading logistics real estate company in Hong Kong has completed construction of a six-story multi-tenant logistics facility in Kawanishi City, Hyogo Prefecture. The facility will be one of Japan's largest logistics facilities, with a total site area of approximately 500,000 square meters. It is one of the leading logistics hubs in the Kansai region, which covers not only the Kansai region but also the broader western Japan area, serving as a logistics base capable of handling the last mile in the Hanshin area, such as from central Osaka to the north and to Kobe City, etc. | April 2025 | 1,300 |

| Saitama | ESR has completed construction of a four-story multi-tenant logistics facility with a site area of approximately 17,000 square meters in Hidaka City, Saitama Prefecture, as its seventh project in the prefecture. Located in a highly accessible area near the center of Saitama Prefecture, the facility can accommodate a wide range of logistics needs, including deliveries not only to the entire Kanto region and Niigata, but also to areas west of Kanto. | September 2024 | 357 | |||

| Tokyo | ESR announced that it would develop its fourth domestic DC in central Tokyo. The planned power receiving capacity is 60MW. Construction is scheduled to begin in the second quarter of 2026 and service to begin in the fourth quarter of 2028. This DC will be the one following those in Osaka City, Osaka Prefecture (130MW), Higashikurume City, Tokyo (30MW), and Soraku-gun, Kyoto Prefecture (100MW). | May 2024 | 357 | |||

| United States | Communications | Ibaraki and Mie | Google announced that it would invest 1 billion US dollars in laying submarine cables in Japan. The plan is to connect the United States and Japan by laying two new submarine cables, Proa and Taihei, and expanding existing submarine cables. | April 2024 | 1,000 | |

| CapitaLand | Singapore | Communications | Osaka | CapitaLand Investment, a major real estate investment company based in Singapore, will develop a DC in Osaka Prefecture. This is the first time the company has engaged in DC business in Japan. The planned power capacity is approximately 50MW and the company announced that it had secured a considerable amount of power supply. | February 2025 | 700 |

| Eku Energy | Australia | Renewable Energy | Miyazaki | Eku Energy, an Australian energy storage company, announced plans for a 30MW/120MWh Battery Energy Storage System (BESS) project to be developed in Miyazaki City, Miyazaki Prefecture. This project is based on a 20-year offtake agreement with Tokyo Gas. Construction began in the second half of 2024 and operations are scheduled to begin in July 2026. The battery is said to be capable of supplying electricity to approximately 63,000 households for four hours. | April 2024 | 604 |

| UI JAPAN | Hong Kong | Real Estate | Shiga | UI JAPAN, a real estate development company with a Hong Kong developer as its parent company, has completed construction of the UI Konan Logistics Center II, a four-story multi-tenant logistics facility with a total floor area of approximately 188,141 square meters in Konan City, Shiga Prefecture. The site area is approximately 99,062 square meters and each floor is approximately 45,000 square meters. The facility can be divided into up to 6 tenants for each floor and totally into 24 tenants. It features high-performance specifications, including up-and-down ramps for large vehicles, a clearance height of 6 meters under the beams, double-sided berths, and a floor load capacity of 2.5 tons per square meter. | June 2025 | 434 |

| Prologis | United States | Real Estate | Aichi | Prologis, a U.S.major logistics real estate company, has decided to develop a multi-tenant logistics facility named Prologis Park Tokai 1 in Tokai City, Aichi Prefecture. The facility comprises four above-ground floors, with a site area of approximately 72,800 square meters and a total floor area of approximately 160,000 square meters. Accessible from central Nagoya in approximately 30 minutes. The groundbreaking ceremony was held in August 2025, with completion scheduled for May 2027. It aims to strengthen the logistics network in the Chubu region. | May 2025 | 434 |

| Aichi | At the same time, the company announced a development plan for Prologis Park Tokai 2, a build-to-suit (BTS) logistics facility designed and constructed to meet requirements of a specific tenant, on an adjacent site to Prologis Park Tokai 1. The facility will comprise four above-ground floors, with a site area of approximately 29,300 square meters and a total floor area of approximately 63,700 square meters. With excellent access to major arterial roads and ports, the facility serves as a strategic hub connecting to the Nagoya metropolitan area. Completion date is yet to be announced. | May 2025 | 434 | |||

| Iwate | Prologis has decided to develop a multi-tenant logistics facility named Prologis Park Kitakami-Kanegasaki in Kanegasaki Town, Isawa-gun, Iwate Prefecture. Located near a major transportation hub, the site offers excellent accessibility to various parts of the Tohoku region. The groundbreaking ceremony was held on June 6, 2024. Completion is scheduled for January 2026. | June 2024 | 357 | |||

| Osaka | Prologis has decided to develop a BTS logistics facility named Prologis Park Sakai in Sakai City, Osaka Prefecture. Designed exclusively for specific companies, the facility will comprise four above-ground floors, with a site area of approximately 17,400 square meters and a total floor area of approximately 37,000 square meters. Located approximately 6 km from the Hanshin Expressway Sakai Interchange, the site offers access to central Osaka City in about 30 minutes and aims to strengthen the wide-area logistics network across the Kansai region. Construction began in 2025 and is scheduled for completion in 2027. | April 2024 | 357 | |||

| Okayama | Prologis has decided to develop a multi-tenant logistics facility named Prologis Park Okayama in Okayama City, Okayama Prefecture. Designed as a general-purpose logistics base that can accommodate multiple companies, the facility has four above-ground floors, with a site area of approximately 16,600 square meters and a total floor area of around 35,000 square meters. Located approximately 9 km from the Kurashiki Interchange and about 3.5 km from the Hayashima Interchange on the Sanyo Expressway, the facility aims to strengthen the wide-area logistics network across the Chugoku and Shikoku regions. The groundbreaking ceremony was held in April 2024 and the facility was completed in August 2025. | April 2024 | 357 | |||

| GLP Japan Development Venture | Singapore | Real Estate | Fukuoka | GLP Japan, a major logistics real estate company headquartered in Singapore, has begun Kyushu's first large-scale development project, the GLP Fukuoka IC Project, in Kasuya-gun, Fukuoka Prefecture. The project consists of multiple logistics facilities with a total floor area of over 150,000 square meters, with construction scheduled to begin in November 2025 and all buildings completed by the end of 2028. This location was selected as it is situated approximately 800 meters from the Fukuoka Interchange on the Kyushu Expressway, making it ideal for wide-area distribution throughout Kyushu. It will function as a critical infrastructure to meet the growing demand for logistics. | April 2025 | 425 |

| Kanagawa | GLP Japan has announced construction plans for GLP Kawasaki II, one of Japan's largest multi-tenant logistics facilities with frozen and refrigerated storage, which is currently under development in Kawasaki City, Kanagawa Prefecture. The facility has a total floor area of approximately 200,000 square meters and a storage capacity of approximately 186,000 tons, featuring not only frozen and refrigerated sections but also ambient-temperature sections. Construction began in March 2025 and is scheduled for completion at the end of August 2027. | October 2024 | 357 | |||

| CBRE Group, Inc. (CBRE) | United States | Real Estate | Hokkaido | CBRE, a U.S. real estate company, has announced plans to develop a large-scale, multi-tenant logistics facility in the Chitose Distribution Business Park in Chitose City, Hokkaido. With a total floor area of 24,500 square meters, the facility will be a three-story steel-frame structure. Construction began in March 2025 and is scheduled to be completed in October 2026. It aims to capture logistics demand related to semiconductors. | October 2024 | 357 |

| Goodman Group | Australia | Real Estate | Ibaraki | Goodman Group, an Australian real estate giant, plans to develop a new DC campus in Japan and provide 1,000MW of power. The company announced that site preparation and infrastructure work were underway in Tsukuba City, Ibaraki Prefecture, with the first DC scheduled for completion in 2026 with a power receiving capacity of 50MW. | January 2024 | 357 |

| LaSalle Investment Management | United States | Real Estate | Aichi | LaSalle Investment Management, a U.S. real estate investment advisory firm, announced that it would build a multi-tenant logistics facility in Nagoya City, Aichi Prefecture, in collaboration with NIPPO. Construction is scheduled for completion in June 2025. In addition to serving as a wide-area distribution center for the entire Tokai area, it is planned to function as a relay center between the Tokyo metropolitan area and the Kansai region. | January 2024 | 357 |

| EdgeConneX | United States | Communications | Osaka | EdgeConneX, a U.S. DC solutions provider, announced plans to enter the Japanese market. The company plans to open a DC campus with a capacity of over 140MW in the Osaka and Kyoto areas by 2027. When completed, the data center will be one of the largest in the Kansai region and will feature a cutting-edge design that meets high-density requirements of AI and high-performance computing. | January 2025 | 273 |

| Zuora | United States | Communications | Uncategorized | Zuora, a U.S. telecommunications company (providing platforms for subscription businesses), has announced the start of operations of its new data center in Japan. The DC is designed to ensure robust compliance with Japan's Act on the Protection of Personal Information and significantly enhance its performance within the country, with the aim of acquiring domestic ISP vendors as clients. | November 2024 | 273 |

| CyrusOne KEP | United States | Communications | Osaka | CyrusOne, a U.S. DC developer and operator, and Kansai Electric Power Co. (KEPCO) have launched their first hyperscale data center project in Seika Town, Kyoto Prefecture. This project marks CyrusOne's first data center construction in Asia and will provide 48MW of IT capacity. Construction will be carried out in three phases, with the first 16 MW phase scheduled to begin operations in the first quarter of 2028. | September 2024 | 273 |

| Empyrion Digital | Singapore | Communications | Tokyo | Empyrion Digital, a Singaporean digital infrastructure platform, announced that it would expand its business footprint in Asia by entering the Tokyo market. Plans include developing a 35MW AI-enabled DC (JP1) in central Tokyo. The DC will be established to support workloads for generative AI and high-performance computing. | September 2024 | 273 |

| Equinix | United States | Communications | Osaka | Equinix, a U.S. company which owns, leases, and provides related services for DCs, has opened its fourth domestic hyperscaler DC, OS4x, in Minoh City, Osaka Prefecture. The center provides a total of 14.4 MW of IT power across 4,926 square meters of data hall space. This DC is designed to meet the growing demand for generative AI. | June 2024 | 273 |

| Vantage Data Centers | United States | Communications | Osaka | Vantage Data Centers, a U.S.-based leading provider of hyperscale DC campus management, announced that it had begun construction of its first campus in Japan, Osaka (KIX1). This campus, to be built in Ibaraki City, Osaka Prefecture, will provide up to 68MW. The campus will support both cloud and high-density implementations, providing hyperscalers and cloud providers with flexibility and scalability to meet market needs. | May 2024 | 273 |

|

GDS Services, Gaw Capital Partners |

China and Hong Kong | Communications | Tokyo | GDS Services, a Chinese company which develops and operates DCs, announced plans to build a 40MW data center in Fuchu City, Tokyo, in collaboration with Hong Kong-based real estate investment firm Gaw Capital Partners. This data center will be located in the Fuchu Intelligent Park and is scheduled to begin operations by the end of 2026. The total site area is 10,969 square meters, and the IT capacity is expected to be 40MW, designed to meet Japan's digital infrastructure demand. | April 2024 | 273 |

| AirTrunk | Australia | Communications | Chiba | AirTrunk, a specialist in hyperscale DCs, has begun construction of a new facility exceeding 40MW in TOK1, one of Japan's largest campuses, located in Inzai City, Chiba Prefecture. The campus covers an area of 13 hectares and is to consist of seven buildings, with a total power supply capacity expected to exceed 300MW. The company plans to have a domestic power supply infrastructure for IT equipment, exceeding 430MW by combining the capacity of TOK1, TOK2 (west of Tokyo), and OSK1 (west of Osaka). | June 2025 | 256 |

| Enfinity Global | United States | Renewable Energy | Aomori | Enfinity Global, a U.S. renewable energy company, has completed construction of a 70MW solar power plant in Aomori Prefecture. This power plant is expected to generate over 75 GW of clean energy annually. Including this solar power plant, the company owns a solar power generation portfolio of 250MW in Japan and is positioned as one of the leading players in the Japanese market. | April 2024 | 195 |

| Invenergy | United States | Renewable Energy | Hokkaido | Invenergy, a U.S. renewable energy company, has begun commercial operation of an onshore wind power plant in Rusutsu Village, Hokkaido. It consists of 15 large wind turbines and has an output of 4.2MW each, totally 63MW. It is expected to reduce carbon emissions by 64,000 tons annually, while supplying electricity to approximately 35,000 households in Hokkaido. | March 2024 | 189 |

-

Note:

Ranked by investment amount based on announcements or media reports (fDi Markets, including estimates).

-

Source:

Based on "fDi Markets" by the Financial Times, and announcements by each company

JETRO Invest Japan Report 2025

-

Section1

-

Section2

-

Section3

-

Section4

-

Section1

-

Section2

-

Section3

-

Section4

-

Section5

-

Section1

-

Section2

-

Section3

Laws and Regulations on Setting Up Business in Japan Pamphlet

The pamphlet "Laws & Regulations" is available in PDF, and outlines basic information about laws, regulations and procedures related to setting up a business in Japan. It is available in English and Japanese. You can download via the "Request Form" button below.

Contact Us

Investing in and collaborating with Japan

We will do our very best to support your business expansion into and within Japan as well as business collaboration with Japanese companies. Please feel free to contact us via the form below for any inquiries.

Inquiry FormJETRO Worldwide

Our network covers over 50 countries worldwide. You can contact us at one of our local offices near you for consultation.

Worldwide Offices