JETRO Invest Japan Report 2023

Chapter2. Trends in Inward FDI in Japan [Column 3] Promotion of More Active and Desirable M&A in Japan

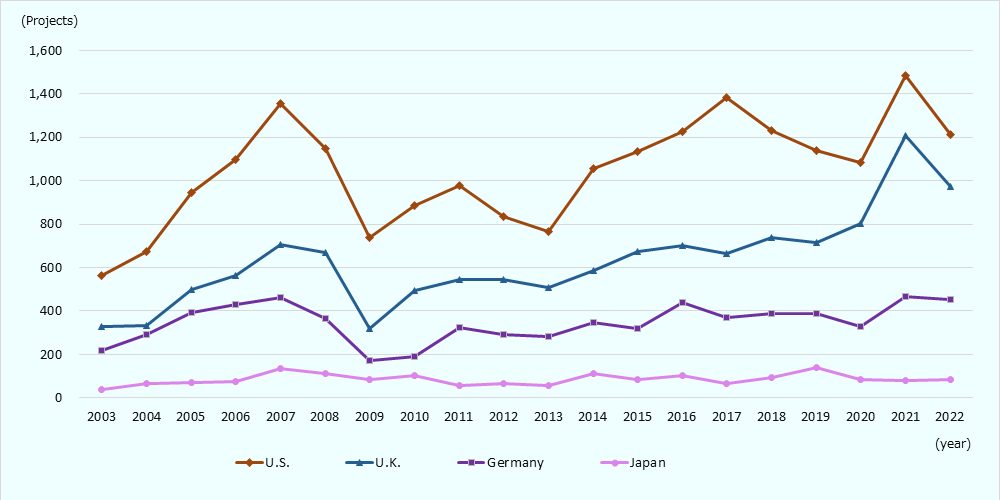

M&A is one of the effective options to achieve speedy and non-consecutive growth in the fierce global competition, and many companies are expanding overseas sales channels, improving management, and strengthening and developing human resources by utilizing global networks and know-hows held by foreign investors. On the other hand, Japan's inward M&A remains at a low level compared to that of other major countries (Chart 2-24). In light of this, in 2023, the Ministry of Economy, Trade and Industry (METI) released the "Case Studies relating to the use of inbound M&A transactions" to publicize it more widely as an option for corporate growth. In addition, METI issued "Guidelines for Corporate Takeovers" to facilitate desirable acquisitions for the economy through the healthy development of market functions in a fair M&A market (Chart 2-25).

Source: The United Nations Conference on Trade and Development (UNCTAD)

Major Benefits for Target Companies That Accepted Foreign Capitals

Management Base

- Sophistication of business and financial management by acquiring global knowledge and management know-how

- Sophistication of business management, promotion of DX, and improvement of productivity/profitability were achieved through incorporating management know-how, expertise, and global standards of governance, in which areas foreign investors are more advanced, such as KPI*1 management, ROIC*2-conscious investment, and business portfolio management.

- Strengthening of the organizational structure through human resources support

- The organizational structure was strengthened through introduction of the most suitable human resources for the issues confronted by the target company, based on the foreign investor's rich personnel networks.

Employees

- Enhancement of employees' motivation through the introduction of a new personnel evaluation system

- Introduction of a new personnel system and a highly transparent evaluation system as well as the grant of stock options and other measures, as used by the foreign investor, contributed to enhancing the employees' motivation.

- Development and strengthening of global human resources

- Training programs and exchanges with global human resources made it possible for the company to develop and strengthen its employees, enabling them to gain a global perspective and mindset. The company became able to recruit more globally-minded human resources, as being under the umbrella of a foreign investor.

Business Operations

- Expansion of the overseas sales channels through a global network

- Expansion of the overseas sales channels was achieved through utilization of the network and brand power of the foreign investor. This contributed to the increase in overseas sales ratio and the expansion of the company's presence in overseas markets.

- Utilization of products, services, and business models in the fields that are more advanced in overseas markets

- Expansion of the range of products and services and quality enhancement were achieved through incorporation of technologies, know-how, and business models related to products and services that are more advanced in overseas markets.

In addition, there are other multiple specific benefits, subject to different case studies. For the target company, benefits may include the optimization of its business portfolio and the securing of funds. For the acquiring party, benefits may include strengthening of ESG and diversity management, progresses in management reforms based on delisting, actively investing in and increasing R&D costs, expanding employment, and carrying out additional M&A transactions, etc.

*1. KPI: Key Performance Indicator. *2. ROIC (Return On Invested Capital)

Source: METI, "Case Studies relating to the use of inbound M&A transactions"

In August 2023, the "Guidelines for Corporate Takeovers" were published. In light of the various changes in the M&A situation in recent years, the purpose of the guidelines is to examine how parties involved should behave regarding acquisitions, and present principles and best practices that should be shared by the parties, to make takeovers that increase corporate value more likely to occur (and those that do not less likely to occur), by improving the predictability and desirability for parties involved in takeovers. Based on the premise that M&A will contribute, in principle, to the enhancement of "corporate value" of Japanese companies by creating synergies through acquisitions and improving inefficient management, etc. *1, actions to take were discussed when an acquirer and a target company have different evaluations of an acquisition proposal. Balancing the interests of both parties, the guidelines as fair rules regarding M&A that should be shared in the Japanese economy and society were created.

Outline (partial excerpt)

The Guidelines present the following three principles that should be respected in acquisitions of corporate control of listed companies in general.

Principle 1: Principle of Corporate Value and Shareholders' Common Interests

Whether or not an acquisition is desirable should be determined on the basis of whether it will secure or enhance corporate value and the shareholders' common interests.

- "Corporate value" represents the sum of the present values of the discounted future cash flows generated by a company, and is explicitly defined as, not qualitative, but a quantitative concept [can be expressed as the sum of shareholder value (market capitalization as valued in the market) and net debt values from the perspective of capital financing sources]. This includes the value arising from quantifiable increases in future cash flows resulting from the contributions by employees, counterparties, and other stakeholders in business activities.

- When a takeover proposal is received, in general, "sincere consideration" is given to a "bona fide offer" (an acquisition proposal that is specific, rationale of purpose, and feasible), and in considering the pros and cons, the acquisition price and other terms of the transaction should be seriously examined (it can be reasonably inferred that a high acquisition price offer is expected to increase corporate value).

Principle 2: Principle of Shareholders' Intent

The rational intent of shareholders should be relied upon in matters involving the corporate control of the company.

- The board of directors of the target company is required to present its own opinion to shareholders, apart from its own interests, as to whether it believes that the proposed acquisition will contribute to enhancing corporate value and securing interests of shareholders, and whether there are other more desirable alternatives.

- Respecting shareholders' intent in an acquisition takes the form of obtaining judgment of shareholders such as through their decision to tender shares or not, and regulatory frameworks are established to ensure that the necessary information (including a statement of opinion by the target company) is available and there is time for the shareholders' judgement. However, in exceptional and limited circumstances where the regulatory frameworks are not considered to be sufficient from the perspective of ensuring transparency, takeover response policies or countermeasures may be applied in response to an acquisition attempt without consent, at the initiative of the company. In such event, it is fundamental to confirm what the reasonable intent of shareholders is at a shareholders' meeting in respect of approval or rejection of takeover response policies and countermeasures in response to such an acquisition attempt.

Principle 3: Principle of Transparency

Information useful for shareholders' decision making should be provided appropriately and proactively by the acquiring party and the target company. To this end, the acquiring party and the target company should ensure transparency regarding the acquisition through compliance of acquisition-related laws and regulations.

-

Note *1:

Acquisitions are made when the acquirer is confident that it will significantly increase the value of the company above the level currently reflected in the stock price. It should be noted that, in addition to the expectation that synergies will enhance value and improve management efficiency through rational behavior in acquisition transactions, the possibility of a takeover will serve as a discipline to current management.

-

Source:

METI "Guidelines for Corporate Takeovers"

JETRO Invest Japan Report 2023

-

Section1.

-

Section2.

-

Section3.

-

Section4.

-

Section1.

-

Section2.

-

Section3.

-

Section4.

-

Section5.

-

Section6.

-

[Column 1]

-

[Column 2]

-

[Column 3]

-

Section1.

-

Section2.

-

Section3.

-

Section4.

-

Section5.

-

Section6.

-

Section7.

-

Section8.

-

Section9.

-

Section10.

Contact Us

Investing in and collaborating with Japan

We will do our very best to support your business expansion into and within Japan as well as business collaboration with Japanese companies. Please feel free to contact us via the form below for any inquiries.

Inquiry FormJETRO Worldwide

Our network covers over 50 countries worldwide. You can contact us at one of our local offices near you for consultation.

Worldwide Offices